Fintech infrastructure in Africa is messy, fragmented and difficult to navigate. And for most fintechs, building their own infrastructure from scratch is not a worthy pursuit.

It is a deeply technical, highly regulated, operationally demanding endeavour where most of the work happens in the background, invisible to everyone except the businesses whose products depend on it running cleanly.

This was the core problem FinCode saw a decade ago and decided to solve by understanding the structural failures holding back digital finance infrastructure behind fintech products, and building the platforms that eliminate those failures.

This is the story of what we have built, who we have powered, and what scaling digital finance in Africa has taught us along the way.

What We’ve Built: A Full-Stack Fintech Infrastructure Platform

The question we set out to answer was straightforward: why do so many promising fintech products in Africa fail to scale. Our finding was: because the fintech backend system beneath them simply cannot hold the weight?

So we set out to build the infrastructure from the ground up, so founders and institutions never have to start from zero again. Here’s what that infrastructure looks like today.

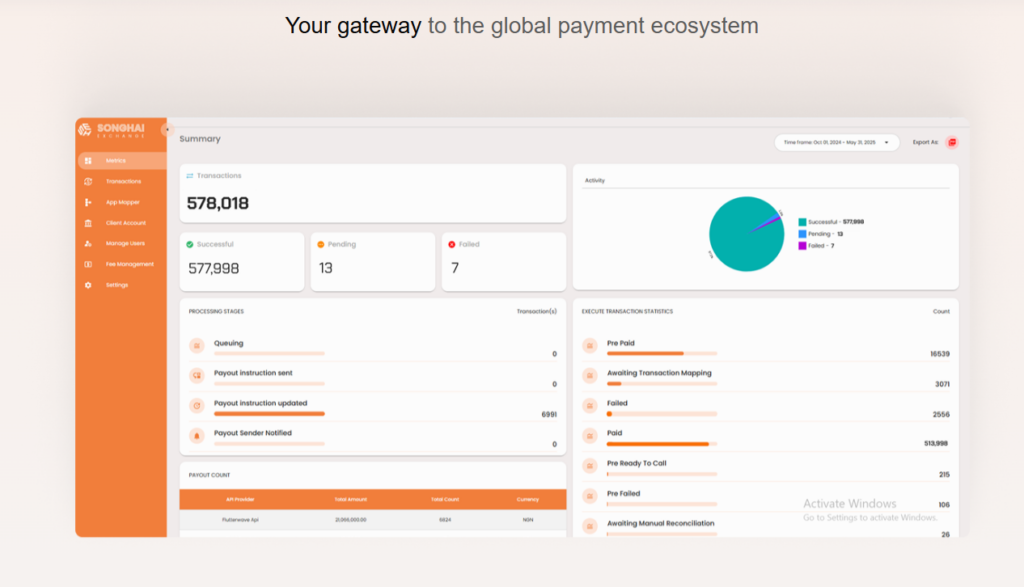

Payment Switch — Songhai Exchange

Our payment switch: Songhai Exchange (SHE) — is a global and domestic settlement and routing platform that connects banks, fintechs, and IMTOs directly to banks and payout partners across 20+ countries through a single API integration. No intermediaries. No unnecessary routing layers eating into your margins.

You own the FX spread, control partner relationships, and get real-time reconciliation across every corridor you operate in. It is, in our estimation, the most important piece of digital finance infrastructure we’ve built — and the one that unlocks everything else.

Songhai Exchange is also recognised among the largest processors of payments to Ghana, and its architecture underpins some of the most significant cross-border payment deployments on the continent. You can read more about how our payment switch helps businesses scale here.

When First Bank of Nigeria needed to connect seven African subsidiaries — spanning anglophone and francophone markets — into a single, coherent cross-border payment solution, they turned to FinCode.

We built the First Global Transfers platform on top of Songhai Exchange: a cross-border payment switching solution that turned what was once a fragmented, multi-day process into settlements that clear in minutes.

CSL Pay, a pan-Africa payment player, needed a scalable cross-border switch to underpin its Pan-Africa payment service. Inefficiencies in payment processing were restricting their growth and cross-border capabilities.

Songhai Exchange solved that — giving CSL Pay the infrastructure to scale operations, reduce transaction times, and position itself as a leader in Pan-African payments. Read the full story here.

Remittance Infrastructure

Launching a remittance business is still harder than it should be. Banking partners, payout networks, compliance frameworks, cross-border rails. The barriers are expensive, slow, and often prohibitive for ambitious founders who could genuinely serve their communities better.

Our remittance infrastructure platform exists to change that equation: giving businesses everything they need — technology, payout corridors, compliance architecture, and operational support — to go live in weeks, not eighteen months.

FCMB, one of Nigeria’s leading financial institutions, engaged FinCode to build a cross-border payment hub connecting the bank to international money transfer operators abroad.

The platform now processes significant volumes of diaspora remittance transactions annually, making it faster and cheaper for Nigerians abroad to send money home — and positioning FCMB as a serious player in the international remittance market.

Beyond powering individual institutions, we extended our remittance infrastructure platform into a product of its own: RemitJunction. A licensed, white-label remittance-as-a-service solution offering businesses a complete launchpad — infrastructure, compliance expertise, licensing framework, and operations, all in one package.

This is Infrastructure-as-a-Service in its truest form: our compliant fintech platform powering other businesses to serve the next layer of fintechs. Read the RemitJunction story.

Digital Wallet and Electronic Money Infrastructure

Our wallet and EMI infrastructure gives businesses the backbone to issue stored-value accounts, run multi-currency wallets, and offer neobanking-grade experiences — without building the underlying compliance and ledger infrastructure from scratch.

The platform handles everything from KYC and AML screening to account issuance, P2P transfers, and settlement.

London-based KogoPAY is one of the clearest examples of this digital finance infrastructure in action. They partnered with FinCode to launch an award-winning multi-currency digital wallet and remittance product in the European market, complete with EMI licensing support, AML compliance workflows, and full integration with a partner bank’s core banking infrastructure.

What would have taken years to build independently was brought to market in a fraction of the time.

Virtual Account and Multi-Currency Management

Modern financial businesses — especially those operating across borders — need to manage multi-currency accounts, automate reconciliation, and issue virtual accounts with precision.

Our fintech backend system for virtual account management supports multi-currency business accounts, internal and external account issuance (IBANs, sort codes, SWIFT/BIC), automated reconciliation, and full cross-border payment support.

Stern Bank needed an all-in-one banking platform through which their clients could make cross-border payments, hold multiple currencies, and access liquidity for trade financing.

FinCode delivered a robust, scalable borderless banking platform — giving Stern Bank the tech to launch online cross-border banking and trade finance services quickly, meeting the needs of SMBs and solidifying their market position.

What Else We’ve Built

Beyond payments, remittance, and wallets, our compliant fintech platform covers the full range of financial products businesses need to serve their customers.

Lending

Lending in Africa is a market full of ambition and, unfortunately, full of risk engines that behave like moody teenagers. Designing a sustainable credit product means getting decisioning right, collections right, and compliance right — simultaneously.

Our lending solution gives organisations the infrastructure to build bespoke digital lending schemes: automated underwriting, repayment management, debt collection workflows, and deep loan accounting — all in one platform. Here’s why compliance-first infrastructure matters specifically for lending businesses.

Savings & Investment, and CIAM

Our savings and investment platform gives businesses the infrastructure to offer goal-based savings, fixed income products, and digital investment features — with full KYC, AML, and reporting built in.

Alongside this, our Customer Identity and Access Management (CIAM) engine provides the control layer that ties everything together: user profiling, compliance configuration, security enforcement, and platform integrations managed from a single interface — so your ops team isn’t dependent on engineering for every configuration change.

Taken together, these are the building blocks of a compliant fintech platform that spans the full spectrum of digital financial services. You can read more about what FinCode’s infrastructure does across all these product lines here.

What We’ve Learned: Lessons From Building Fintech Infrastructure in Africa

A decade of building fintech infrastructure in Africa leaves you with a very specific kind of knowledge — the kind you can’t read in a textbook or absorb from a conference panel.

Here are the most important lessons from building fintech infrastructure across this market:

1. The rails matter more than the UI

The most common point of failure we have witnessed is not bad design or weak product-market fit. It is infrastructure that breaks under volume, compliance engines that can’t adapt to regulatory changes, and payment rails that were bolted together rather than engineered for scale.

2. Compliance is a feature, not a legal obligation

The fintechs that scale confidently across Africa treat compliance as a competitive advantage. They build compliant fintech platform architecture from day one, so regulatory changes don’t require product rebuilds.

3. Infrastructure partnerships change the economics of fintech investing

This one is particularly relevant for the investor community. When a startup launches on proven digital finance infrastructure, the risk profile changes fundamentally. We’ve written more on how infrastructure partnerships de-risk fintech investments here. It’s reading we’d recommend to any VC with African fintech exposure.

4. Multi-tenancy is not optional at scale

Running multiple fintech products on shared infrastructure is a genuine superpower — if the architecture supports it properly. Full tenant isolation, configurable business logic per client, and performance that doesn’t degrade as the tenant count grows are non-negotiable.

This is something we engineered into FinCode from the beginning. Here’s a deeper look at how our multi-tenancy infrastructure works.

A Decade In. Just Getting Started.

FinCode has spent ten years becoming exactly that partner for banks, MFIs, fintechs, and money service businesses across Africa and beyond. We’ve built the rails. We’ve powered the products.

And we’ve accumulated the kind of hard-won lessons from building fintech infrastructure that only come from being in production — not just in planning — for a decade.If you are building, scaling, or investing in digital finance infrastructure in Africa, we’d like to talk. Reach out to the FinCode team here.