If you’ve spent any time building or running a remittance business, you already know the feeling. You get a product to market in one corridor, onboard your first few thousand users, and achieve some early traction. But when it’s time to scale to a new market, you realise a painful roadblock: building compliance all over again for the specific market.

What this looks like in practice is corresponding with regulators in the new region you’re scaling into, engineering new compliance frameworks into your product, acquiring new licenses (if needed), building local institutional partnerships and network of local payout operators.

And that is just to go-live in a new country.

Scaling remittance corridors compliantly, especially across Africa, is one of the most structurally complex things a fintech can attempt. Yet it is also one of the highest-value opportunities available.

The largest remittance corridors globally run through Africa: Nigeria, Ghana, Kenya, Senegal, the Gambia, and increasingly, countries like Rwanda and Côte d’Ivoire. The UK–Africa remittance corridor alone moves billions of pounds annually, fuelled by one of the world’s largest African diaspora populations. The numbers are not in dispute. But the path to capturing them responsibly is where most remittance startups hit a wall.

This piece is about that wall; why it exists, what it actually costs to climb it manually, and how FinCode’s compliant cross-border infrastructure is changing the economics and speed of corridor expansion for remittance businesses.

The Compliance Architecture Beneath Every Remittance Corridor

Compliantly scaling remittance corridors is more than just a legal exercise. It is largely an infrastructure problem.

To operate in any corridor — say, UK to Nigeria, you need licensing or an authorised agent relationship in both jurisdictions, AML for cross-border payments that satisfies both the FCA and the CBN, KYB verification for your business entity in each market, reliable local banking rails for settlement, and a payout partner network that can actually deliver funds to the end beneficiary at competitive rates.

Now multiply that across five corridors. Or ten. Each country has its own regulatory body, its own KYC tiering requirements, its own AML rules for cross-border payments, its own local banking relationships to build, and its own definition of what “compliant” looks like in practice.

The largest remittance corridors in Africa — UK to Nigeria, US to Ghana, EU to Senegal, intra-Africa between Kenya and Uganda, are each individually sophisticated. Running multiple corridors in parallel, without a shared compliance architecture beneath them, is a sure fire way to burn capital and miss windows.

And the operational cost of getting this wrong is heavy. A missed filing, an incomplete AML check, or a settlement partner that doesn’t meet local regulatory requirements, can ground your entire operation in that market. Cross-border payment regulations are not forgiving on the timeline side. Regulators expect businesses to be operationally ready before they go live, not compliant by approximation.

How FinCode Powers Corridor Scale Without Rebuilding Compliance from Scratch

Here is where the conversation shifts from problem-framing to solution architecture, specifically, to how FinCode’s remittance and switching infrastructure changes what is possible for scaling remittance startups.

FinCode’s compliance engines were built as part of the foundation of our fintech infrastructure for African banks, money service businesses and fintech startups. What this means is that we have already done the heavy lifting of establishing the regulatory relationships (extensively across multiple markets), licensing arrangements, banking rails, and AML for cross-border payments frameworks in each of those markets.

Businesses launching on top of our infrastructure, whether it’s a remittance startup building their first product or a bank extending its diaspora services, can benefit from everything we have built without having to rebuild it from zero.

Read More: Learn more about what FinCode actually does at the infrastructure level.

Configuring a New Corridor Without Rebuilding Compliance from Scratch

Here is the practical version of how this works. A remittance business built on FinCode launches in Nigeria. They configure their compliance workflows for the Nigerian market through their FinCode back-office: KYC tiers, AML transaction monitoring thresholds, settlement partner routing, and fee structures. Then they go live.

Six months later, they want to expand to the Gambia, a corridor with strong UK diaspora demand but one that most remittance platforms find difficult to serve profitably because of the compliance overhead. Traditionally, entering the Gambia would mean sourcing new banking partners, engaging a local compliance consultant, obtaining or aligning with a licensed entity, and integrating new settlement rails, a process that takes months and meaningful capital.

On FinCode, the process looks fundamentally different. Because we are already live and operational in the Gambia, the compliance infrastructure is already in place. The business logs into their FinCode back-office and configures compliance parameters for the Gambian market: local KYC requirements, AML rules calibrated to the regulatory framework, payout routing to our established local partners. Weeks, not months. Real operations, not a pilot.

The same business can then plan expansion to South Africa, or Ghana, or the UK, and for every supported country, the model repeats.

Scaling remittance corridors compliantly becomes a back-office configuration exercise rather than an eighteen-month infrastructure build. This is precisely how compliant cross-border fintech infrastructure is supposed to work.

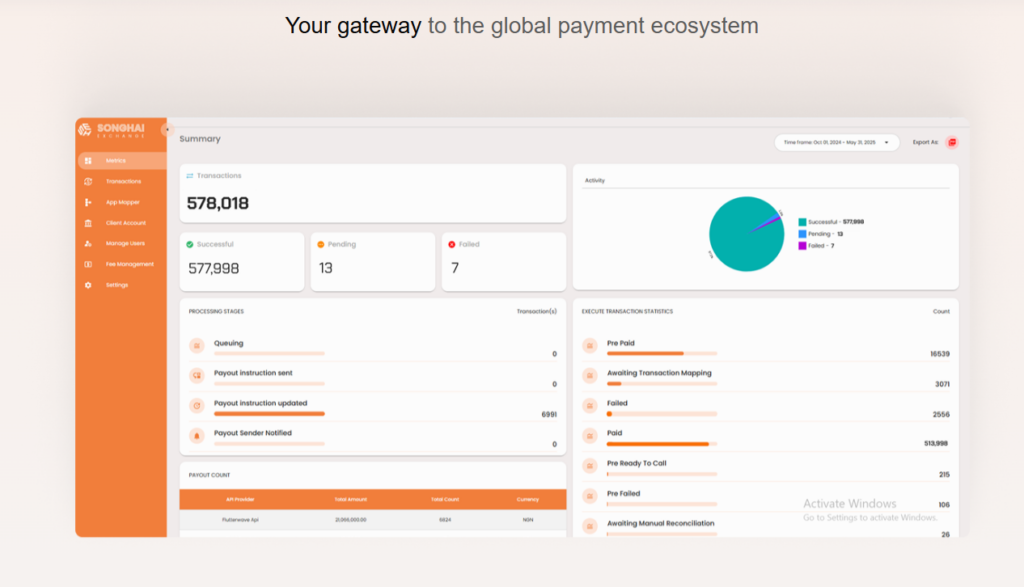

The Payment Switch Beneath It All: Songhai Exchange

Underlying the entire compliance layer is our payment switching infrastructure, Songhai Exchange. If you want to understand how remittance businesses truly scale, you need to understand what payment switching really means for scale.

The payment switch is what handles transaction routing across payout corridors, real-time settlement reconciliation, FX margin management, and exception handling when a partner has downtime. It is the operational brain that makes cross-border payments work reliably at volume, across multiple corridors simultaneously, without requiring your team to manually manage each one.

Songhai Exchange connects businesses directly to banks and local payout partners without intermediaries sitting in the middle taking margin. When you process a remittance through FinCode, you own the FX spread, you see the settlement in real time, and you have full visibility into every transaction state. For remittance product managers, that level of transparency is what makes corridor economics viable.

The Risk of Fragmented Expansion

Let’s be clear about what the alternative looks like, because many remittance startups still take the fragmented approach, building compliance independently for each corridor they enter. The consequences are well-documented, even if not always publicly.

Regulatory compliance fintech failure is rarely dramatic and public; it tends to be slow and expensive. A business that builds compliance for Nigeria independently, then builds it again for the UK, then again for Ghana, ends up with three disconnected compliance architectures that cannot share data intelligently, cannot adapt quickly to regulatory changes, and require three separate sets of banking relationships to maintain. Each corridor becomes its own operational burden rather than an extension of a shared system.

This fragmentation also creates investor concerns. Remittance businesses seeking Series A or growth capital are increasingly asked how they manage regulatory compliance fintech risk across markets, and “we handle each country separately” is not the answer that instills confidence.

Read More: Why VCs are increasingly partnering with infrastructure-backed fintechs.

There is also the question of what happens when regulations change, and in Africa, they do change, sometimes quickly. A business with a shared, configurable compliance infrastructure can update its AML thresholds or KYC requirements centrally, across all active corridors, as regulatory requirements evolve.

A business with fragmented compliance has to make those changes market by market, often under time pressure. One of these businesses can respond to regulatory shifts like a professional. The other responds like a startup that outgrew its original architecture.

The Infrastructure Partnership Model and What It Changes

FinCode’s approach to remittance infrastructure is continuous. We stay involved after launch: monitoring compliance, supporting settlement operations, helping scale payout networks, and ensuring that every corridor a business enters on our platform is one they can actually operate sustainably.

For those interested in the broader framing, how infrastructure partnerships de-risk fintech at scale captures the model well. The short version: when your infrastructure partner has skin in the game, you are not navigating compliance uncertainty alone.

This matters especially for remittance businesses exploring how to expand remittance corridors in Africa. Africa is not one market. It has 54 regulatory environments, dozens of local banking ecosystems, and varying payout network maturity, all layered on top of strong and growing remittance demand.

The businesses that will win the largest remittance corridors in the next five years are not the ones with the most capital. They are the ones whose infrastructure allows them to move into new markets faster, with lower compliance risk, and without burning their engineering teams on regulatory plumbing.

What Scaling Remittance Corridors Compliantly Actually Looks Like

There is a version of this story that sounds abstract until you see it in practice. A remittance startup building on FinCode has access, from day one, to our compliance engine, our payout partner network, our AML for cross-border payments infrastructure, and our banking relationships in supported countries. They launch. They grow.

And when they want to expand corridors in Africa, whether into West Africa, or within East Africa, or across the diaspora routes that matter to their customers, it’s a matter of configuring the compliance requirements of the new corridor in the back-office.

That is a different kind of competitive advantage. And for remittance startups that have found product-market fit in one corridor and are ready to scale in the next five, the infrastructure decision is the most important one they will make.

Choosing to build compliance from scratch at every step is a choice to be perpetually behind the market. Choosing infrastructure that carries compliance as a native capability is a choice to compete.If you are building or scaling a remittance business in Africa and you want to understand what launching on FinCode’s infrastructure actually looks like for your specific product, get in touch with us here. We would rather spend time showing you the platform than convincing you it exists.